The dominance of large chains in the retail landscape is hard to ignore. Casual observation of every city in North America, large or small, often has an eerily similar configuration of clothing, convenience, food, and general-purpose vendors. As The Economist aptly pointed out, there is often “an overwhelming sense of déjà vu” when navigating a retail environment. The feverish growth of retail chain stores has not gone unnoticed by researchers, as large chains grow at faster rates than small chains (Basker, Klimek, and Van, 2012; Blevins, Khwaja, and Yang, 2018). Overly saturated markets with the same set of chains are a potential policy issue. From an antitrust perspective, dominance of the largest retail chains might deter entrants from competing (Fang and Yang, 2022; Fang and Yang, 2023a, 2023b, Igami and Yang, 2016, Nishida and Yang, 2020), and for urban development, markets with little variety in retail amenities might be less attractive for prospective residents (Couture and Handbury, 2020).

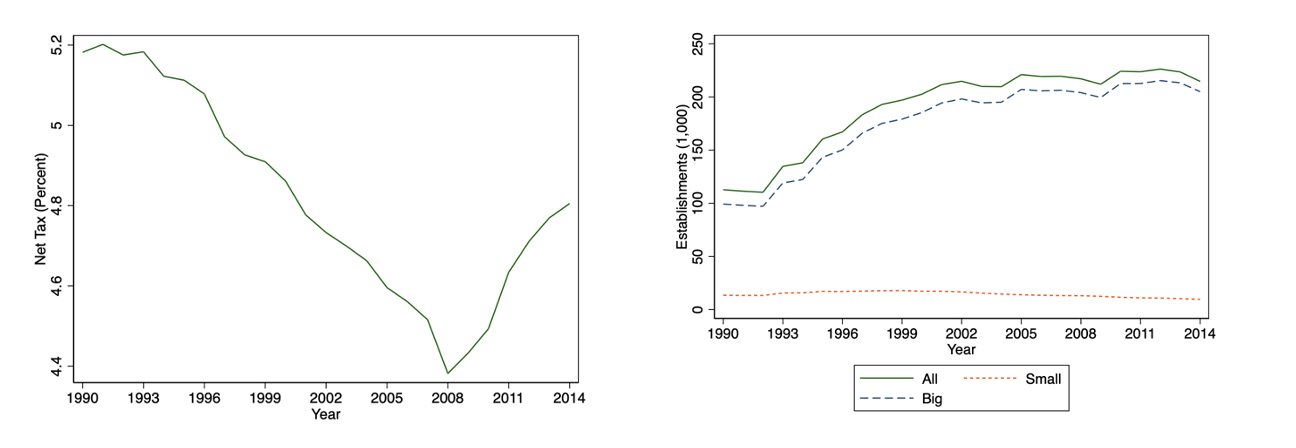

Retail chains likely have intrinsic advantages such as scale economies (Holmes, 2011; Jia, 2008), within-network inventory flexibility (Ergin, Gumus, and Yang, 2022), branding/reputation (Hollenbeck, 2017), technology adoption (Basker, 2012), and superior market data/information (Chi, 2023, Yang, 2020). While these advantages could relate to hard-earned internal capabilities, antitrust and urban policy makers might want to understand to what extent the policy environment is particularly favorable to the largest chains. We ask this question as correlational patterns (see figure below) seem to suggest that the trend of decreasing net taxes at the state level (tied to entry costs) coincide with trending growth among the largest retail chains. Our recent study aims to answer this question. Theoretically, tax policies on entry costs can impact firms asymmetrically depending on how much market share they are able to secure upon entry, whereby large retail chains often arrive at local markets with built-in brand recognition and/or more aggressive pricing power.

This question is not trivial, as it’s likely that state tax policies might be designed with an projection about how much the industry will grow in the future. To address this methodological challenge, we use large-scale data that captures the dynamics of retail establishment (from 1990 to 2014) and focus our analysis on local markets (i.e., counties) that are adjacent to state borders. The intuition behind this research design is that contiguous markets on each side of the border likely face similar underlying economic conditions and different state tax conditions depending on which side of the border they are on. This research strategy is known as a spatial discontinuity approach (Dell, 2010; Holmes, 1998) and is now applied in many different empirical settings.

Our empirical analysis reveals a few important insights. First, perhaps not surprisingly, we find that lower net taxes will in general stimulate the entry of retail establishments; conversely, higher taxes (which is what we do not see in the data) might actually increase competition and break the dominance of large chains. Second, and most importantly, this retail establishment growth appears to be driven almost exclusively by the largest retail chains (i.e., those with 40 or more locations). Consequently, local markets that have lower net taxes appear to have a retail landscape dominated by a small number of large retail chains. One way of interpreting these findings is that uniform tax policies will be amplified (i.e., negative responses to higher taxes, positive responses to lower taxes) by the firm’s size, in that the largest retail firms are most responsive to taxes, good or bad. Ultimately, favorable (and seemingly uniform) state tax policies aimed at encouraging entry might (perhaps unintentionally) help large chains become even more dominant.

Feng Chi is a PhD Candidate in Applied Economics at Cornell University, SC Johnson College of Business

Limin Fang is an Assistant Professor of Strategy and Business Economics at the University of British Columbia, Sauder School of Business

Mengwei Lin is a PhD Candidate in Applied Economics at Cornell University, SC Johnson College of Business

Nathan Yang is an Assistant Professor of Marketing at Cornell University, SC Johnson College of Business

This post was adapted from their paper, “A Tax-Shaped Retail Landscape,” available on SSRN.