Over the last decade, there has been a significant increase in the popularity of socially responsible investment (SRI) funds. These funds claim to incorporate environmental and social (E&S) risks into the selection of their portfolio firms and the majority of these funds also claim that they engage with their portfolio firms to improve the real-world behavior of firms. Yet, it is unclear whether these funds deliver on their promises, and in particular, whether their efforts cause firms to act more responsibly along environmental and social dimensions. In our forthcoming Review of Finance paper, we provide new evidence on the role of SRI funds in society. In particular, we examine whether SRI funds (1) select firms with better E&S behavior and (2) successfully work to improve firm E&S behavior.

Over 80% of SRI funds have a stated mandate to actively impact their portfolio firms’ E&S behavior. Further, these funds often advertise themselves as having environmental and social goals and in many cases the fund’s name alludes to these goals. As a result, investors in these funds expect them to improve corporate conduct (Levine, 2021). Yet to date, it is unclear how effective SRI funds are at bringing about environmental and social change. Theoretically, the results could go either way. On the one hand, the recent increase in the amount of investors’ capital in SRI funds could make them effective at influencing firm behavior through the threat of exit or through voting and engagement. On the other hand, the cost of engaging with portfolio firms and changing their behavior is clearly higher than the cost of simple, static portfolio selection based on firms’ observable E&S performance. Simply put, such engagement requires a tremendous amount of resources and expertise. Thus, SRI funds may lack the incentive to engage as well as the expertise, resources, or stewardship personnel (e.g., Bebchuk and Tallarita, 2020).

These opposing forces make it unclear, ex-ante, what SRI funds actually do. We see three main possibilities:

- SRI funds might behave similarly to non-SRI funds in both selection and impact (i.e., “greenwashing”). That is, they “talk that talk” but do nothing, or almost nothing in terms of investing in firms that are better on the E&S dimension, nor do they impact firms’ behavior along these dimensions.

- SRI funds might select firms with better E&S performance, but make no impact on firm behavior (“impact washing”); or

- SRI funds might successfully improve the E&S performance of their portfolio firms.

To settle the question, we examine whether (i) SRI funds choose firms with good environmental and social conduct and whether (ii) they cause their portfolio firms to improve environmental and social conduct.

To examine the real-world impact of SRI funds, we collect comprehensive data on the environmental and social conduct of U.S. firms from 2010 to 2019. Specifically, we collect and examine 18 different measures. On the environmental dimension, we examine seven measures using data from the Environmental Protection Agency (EPA) that include carbon emissions, toxic releases, and investment to reduce future pollution. On the social dimension, we examine two measures of workplace safety using data from the Occupational Safety and Health Administration (OSHA), two measures of diversity on the board of directors using data from BoardEx and ISS, and seven measures of employee satisfaction using data from Glassdoor.

We find evidence that SRI funds do select companies with better environmental and social conduct. On average, SRI funds hold firms that pollute significantly less. Moreover, SRI funds hold firms that have higher employee satisfaction and fewer workplace accidents. Finally, firms in SRI funds’ portfolios have greater gender diversity on the board of directors. In sum, SRI funds offer their investors a portfolio of firms with higher environmental and social standards.

However, we find that SRI funds do not improve the environmental or social conduct of their portfolio firms. We develop a new research design that allows us to examine plausibly random variation in SRI fund ownership. Specifically, we use an increase in funds’ flow due only to the Morningstar rating system, and hence not related to fund manager’s ability or underlying firm characteristics. Our methodology is explained in detail in the paper. Using this approach, we find that changes in SRI fund ownership are followed by zero improvements in their portfolio firms’ environmental or social conduct. In additional tests, we verify that these zero findings are not due to statistical issues or insufficiently long horizons. SRI fund investment reliably has no effect on the conduct of their portfolio firms. In sum, the zero real-world impact of SRI funds is inconsistent with their claimed impact.

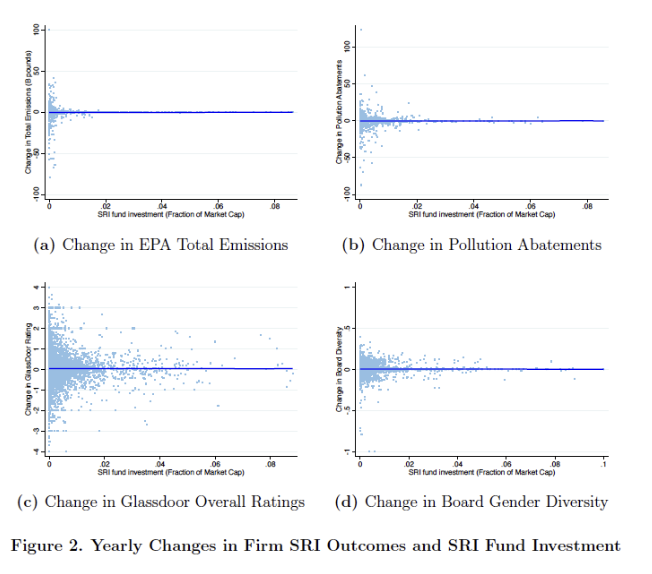

Figure 2 of our paper, reproduced above, highlights these results. We plot the relation between changes in investment from SRI funds and changes in firm behavior along four dimensions: EPA emissions (Panel A), investment in pollution abatement technology (Panel B), employee satisfaction as measured by Glassdoor reviews (Panel C), and gender diversity on the board of directors (Panel D). In each panel, we also plot a best fit line. In all four panels, the best fit line is almost perfectly horizontal, indicating that higher investment from SRI funds is not associated with changes in firm behavior.

Overall, all our results point to the same conclusion: SRI funds operate primarily as stock selectors, but they do not have real effects on their portfolio firms. While the majority of SRI funds have stated goals of selecting better behaved firms and improving firms’ conduct, we find they only succeed at the former. In fact, we do not find any evidence they even seriously attempt to impact portfolio firms’ behavior along the E&S aspects. Our results are consistent with predictions in Edmans et al. (2022) that static selection strategies are not effective in promoting socially responsible behavior; according to Edmans et al. (2022), SRI investors should tilt their portfolios towards “brown” stocks that have taken corrective actions to reward companies for improving their behavior. In contrast, we find SRI funds currently invest in “greener” stocks that already behave in a more responsible manner.

Overall, our research suggests that SRI funds do not have the resources and incentives to affect firm-level E&S behavior. At the same time, these funds do have the incentive to appear green since investors allocate more capital to greener funds (Hartzmark and Sussman 2019). However, it is also evident that investor flows respond mainly to third-party ESG ratings. As a consequence, SRI fund managers have weak incentives to exert costly effort to improve firm behavior and, instead, they might prefer to simply invest in stocks that have high ESG ratings from third-party rating agencies. These findings are relevant to both investors in SRI funds and regulators. Future research should consider whether changes to reporting requirements and to the current regulatory structure could allow SRI funds to improve the behavior of their portfolio firms in a more meaningful way.

Davidson Heath is an Assistant Professor of Finance at the David Eccles School of Business, University of Utah.

Daniele Macciocchi is an Assistant Professor at the University of Miami Herbert Business School.

Roni Michaely is a Professor of Finance and Entrepreneurship at the University of Hong Kong.

Mathew Ringgenberg is an Associate Professor of Finance at the David Eccles School of Business, University of Utah.

This post was adapted from their paper, “Does Socially Responsible Investing Change Firm Behavior?,” forthcoming in the Review of Finance and available on SSRN.