Modern capital markets facilitate the separation of ownership and control. This allows shareholders to diversify their portfolios and firms to undertake value-generating projects regardless of their level of idiosyncratic risk. However, the universal push for diversification often means that shareholders do not bear sufficient risk to incentivize them to monitor the firms in their portfolios. As a result, the managers running the firms on behalf of diversified shareholders may pursue private benefits.

The corporate governance literature generally focuses on those institutional investors with the largest ownership stakes in firms (so-called “blockholders”). However, this focus disregards the effect of diversification. In practice, big blockholders, like BlackRock, Vanguard, and State Street, often hold large stakes in thousands of firms, making them highly diversified and—as argued by the literature on common ownership—disinclined to monitor.

In contrast, surprisingly little work exists investigating the monitoring value of smaller but undiversified institutional investors, investors that, through their concentrated bets, have a lot to gain from their monitoring efforts. My research helps fill this gap by investigating institutional investors with large proportions of their portfolio allocated to a firm, which I term high “Portfolio at Risk” (PAR) institutions.

I provide three main findings. First, textual analysis of over 200,000 corporate conference calls shows that higher PAR is associated with greater shareholder engagement. Smaller institutional investors with high PAR engage as much, if not more, as blockholders with low PAR. Second, I document that an increase in PAR by a firm’s top five PAR institutional investors is, on average, associated with an economically meaningful increase in operating profits and market valuations of $34 million and $731 million. Third, I use a law change in Delaware to provide a direct link between the role of undiversified monitoring of high-PAR institutional investors and corporate performance.

Details on empirical findings

To document my first finding, I measure shareholder engagement. Prior research documents that public campaigns by activist investors are very costly and, therefore, relatively rare. Similarly, we know that institutional investors interact with managers of the firms in their portfolios mostly “behind the scenes.” Corporate conference calls provide a notable exception: they are relatively cheap, recurring, and public. Therefore, I use textual analysis to measure shareholder engagement of institutional investors in the transcripts of corporate conference calls. I document a positive relationship between higher PAR and the engagement of high-PAR institutions. However, I do not find such a relationship between larger ownership stakes and the engagement of blockholders. This finding indicates that higher PAR (i.e., lower diversification) is a key determinant for institutional shareholder engagement and that high-PAR investors are important corporate monitors.

To document my second finding, I analyze 150,000 firm-quarter observations for the relation between high-PAR institutional investors and firm performance. I find that an increase in PAR by a firm’s top five PAR institutional investors is associated with an economically meaningful increase in operating profits and market valuations. To better understand what drives this finding, I employ the DuPont decomposition, according to which Operating Profitability = Operating Efficiency × Asset Efficiency. I document that an increase in PAR by a firm’s top five PAR institutions is strongly associated with a significant increase in Operating Efficiency (i.e., cost savings) but only weakly associated with an increase in Asset Efficiency (i.e., sales generation). These findings are consistent with high-PAR institutional investors being effective corporate monitors, reducing agency problems, and subjecting management to heightened market discipline.

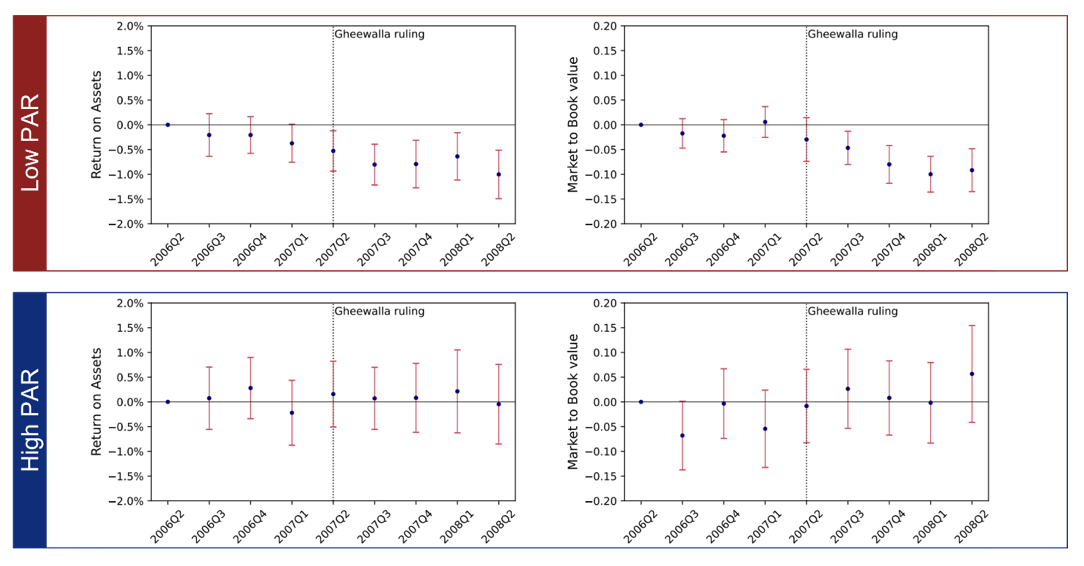

To document my third finding, I use a 2007 law change in Delaware that reduces the role that the monitoring by creditors (i.e., banks, bondholders, etc.) plays for firms (the “Gheewalla ruling”). For the subset of US firms with high creditor monitoring before the Gheewalla ruling, I then compare firms incorporated in Delaware to firms incorporated in other states. After the Gheewalla ruling, I find a decline in profits and valuations for firms in Delaware compared to firms in other states. However, as shown in Figure 1, this result holds only in the subset comparing Delaware and non-Delaware firms that low-PAR investors own. For firms owned by high-PAR investors, there is no difference in performance between those in Delaware and those in other states. This finding corroborates the positive effect of high-PAR monitoring on firm performance. This is because only firms with low-PAR monitoring exhibit deteriorating performance in response to the reduction in creditor monitoring.

Figure 1: This figure presents the dynamic difference-in-differences estimates of the May 2007 North American Catholic Educational Programming Foundation, Inc. v. Gheewalla ruling (Gheewalla ruling) in Delaware (DE), a plausibly exogenous reduction in creditor monitoring in DE, on Return on Assets (operating profitability) and Market to Book value (market valuation). In blue, the coefficient estimates document how firms incorporated in Delaware perform compared to firms incorporated in other states around the Gheewalla ruling. The top row is designated Low PAR and reports firms below the median of the top five PAR institutions’ average PAR, measured at the beginning of each quarter but excluding firms that change their designations at any time over the investigated period. The bottom row is designated High PAR and reports firms above the median of the top five PAR institutions’ average PAR, measured at the beginning of each quarter but excluding firms that change their designations at any time over the investigated period. Control variables are stock return, log of total assets, debt, investment expenses, research & development expenses, sales growth, ownership of top five blockholders, and ownership by insiders, normalized by shares outstanding. All covariates are lagged by one quarter. Due to year-quarter and firm fixed effects, regression coefficients identify within-firm variation. In red, 95% confidence intervals around the coefficients based on heteroskedasticity-robust standard errors adjusted for clustering by the interaction of state-year-quarter are presented.

Implications for researchers and lawmakers

These findings suggest revisiting much extant academic and policy work concerning the drivers and implications of institutional shareholder engagement. Extant academic work focuses on institutional investors with large ownership stakes (blockholders) and finds either no, or a negative, relation with firm performance. However, my findings suggest that for institutional investors, it is not the size of their ownership stakes but their PAR that incentivizes performance-enhancing shareholder engagement. As a result, existing research that does not control for institutional shareholder engagement using the PAR measure is ultimately incomplete.

Extant policy work focuses on index and mutual funds’ transparency vis-à-vis costs and portfolio holdings while mandating—and thus expecting—them to be informed monitors, e.g., through proxy-voting at shareholder meetings (17 CFR § 270.30b1-4). However, my findings show that it is not diversified institutional investors operating in an industry focused on cost-minimization that undertake performance-enhancing (but costly) monitoring efforts. Instead, high-PAR investors undertake such performance-enhancing shareholder engagement, having a lot to gain from their monitoring efforts due to their concentrated bets. As a result, my findings suggest a refocus away from policies that impose governance efforts onto large asset managers toward policies that facilitate the monitoring efforts of smaller institutional investors. Eventually, academics, capital allocators (such as pension funds), and lawmakers must consider the governance role of smaller but undiversified institutional investors. These undiversified institutions counter the rise in diversification-driven shareholder passivity, bringing about positive real economic effects.

Felix Nockher is a Doctoral Candidate in Finance at the Wharton School of the University of Pennsylvania.

This post was adapted from his paper, “The Value of Undiversified Shareholder Engagement,” available on SSRN.