In the first half of 2022, Bitcoin lost over half its value, and the correlation with the stock market jumped to over 60%. These patterns are both remarkable and hard to explain. Why do monetary policy, the economy, or wars matter for the value of cryptocurrencies? Why do cryptocurrencies behave like tech stocks?

From an academic perspective, a correlation between two assets is generally due to the exposure to a common risk factor. In other words, the cash flows generated by the two assets depend, at least in part, on a common underlying reality. Typical risk factors can be the state of the economy, monetary policy, or exposure to specific technologies. For example, the massive simultaneous crash in equity markets in the first half of 2022 is due to the Fed tightening its monetary policy. The impact on tech and growth stocks was stronger, as their valuation strongly depends on cash flows further away in the future.

The risk factors that determine the price of cryptocurrencies is an open question. Major cryptocurrencies like Bitcoin and Ethereum do not have cash flows, meaning that there is no obvious reason for which they should be affected by interest rates or recessions. They do not pay dividends, do not do buybacks, and give no right to real assets. Until recently, commentators discussed the properties of cryptocurrencies as being akin to an inflation-hedge. The idea is to see cryptocurrency as an alternative to fiat currency, and, as such, their limited supply would increase their value when fiat currencies depreciated (i.e., when there is high inflation). The past few months completely disproved this narrative, as cryptocurrencies came crashing down when inflation surged.

In a recent paper, we argue that the reason for this high correlation between cryptocurrencies and equities lies in the trading habits of retail investors. Our key finding is that retail investors buy and sell stocks simultaneously and in the same direction. We show that these correlated trading flows can theoretically cause the correlation we observe between cryptocurrencies and equities. Furthermore, we show that the stocks preferred by crypto-oriented retail investors are the ones experiencing a higher correlation with cryptocurrencies.

For our analysis, we use a unique dataset provided by the quantitative asset management department of the Swiss bank Swissquote. Switzerland has crypto-friendly regulations and is home to many crypto startups and blockchain-based projects. For instance, canton Zug and canton Ticino are among the few public institutions worldwide to accept Bitcoin for certain payments (e.g., fines, local taxes), and various cantons use the Swiss Trust Blockchain to issue official documents. Furthermore, the Swiss government sponsors the Crypto Valley Association, an institution tasked with advocating for the adoption of blockchain technology and developing an ecosystem of crypto-based firms in Switzerland. The crypto-friendly approach of Swiss policymakers allows Swissquote to be among the very few institutional banks worldwide to offer cryptocurrency wallets and operate a cryptocurrency exchange alongside its traditional brokerage services. Our dataset includes daily holdings and trading data of a random subsample of 77,364 Swissquote customers between 2017 and 2020, as well as demographic data (e.g., gender, age, etc.).

We start our analysis by examining how retail investors introduce cryptocurrencies into their portfolios. They tend to reduce their cash holdings and log in much more frequently on the platform. Their overall performance increases, even though the risk-adjusted performance goes down. These results largely depend on the positive performance of cryptocurrencies over the sample period. Interestingly, the performance of the non-crypto part of the portfolio improves, even in risk-adjusted terms. A possible explanation is a reduction in stock trading and in the percentage of short-term trades. In other words, while investors’ overall attention increases after they start trading cryptocurrencies, they tend to pay less attention to stocks and do less short-term trading.

This attention-tradeoff does not mean they stop trading stocks. Not only do they keep trading traditional assets, but they tend to trade stocks and cryptocurrencies at the same time. Periods with intense cryptocurrency trading coincide with periods of intense stock trading. This pattern could have two possible explanations. First, it can be caused by retail investors rebalancing, meaning they sell one asset to buy another. Second, it can be caused by investors’ swinging moods, thus selling and buying both asset classes simultaneously. We look at the correlation between net order flows and indeed find that the two net flows are positively correlated. This positive correlation corroborates the idea that investors somehow see cryptocurrencies as akin to stocks and trade them simultaneously and in the same direction.

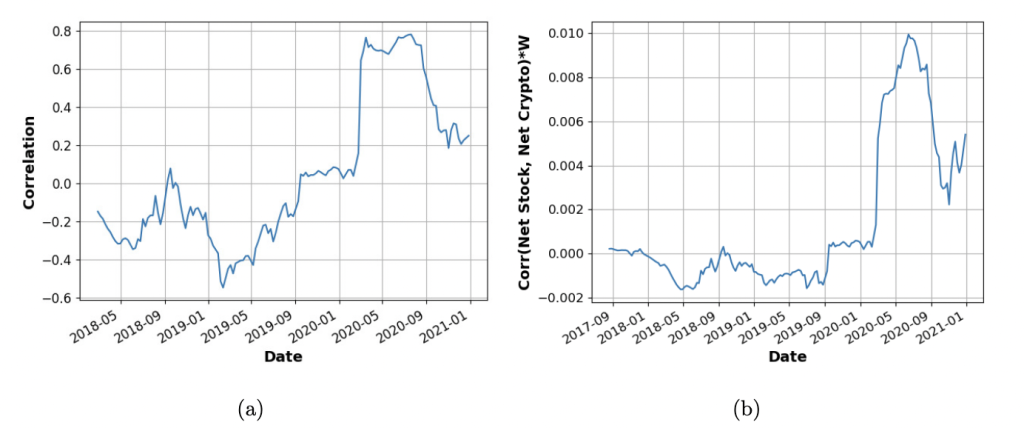

We develop a simple theoretical model, based on Kyle (1985), to show that this correlation in net order flows can theoretically translate into price correlation. Given this theoretical framework, we derive some implications to test in the data. First, we should observe a regime change in the cross-asset retail investors’ trading habits in Spring 2020, when the persistent positive correlation between cryptocurrencies and equities started. Second, periods where retail traders are active in the cryptocurrency market should be associated with a higher cryptocurrency-equities correlation. Third, this mechanism should be stronger on stocks preferred by crypto-oriented retail investors.

Looking at the correlation between net flows, we find that it skyrockets in Spring 2020, especially more so if weighted by trading volumes. While this observation does not prove causality, it strongly suggests a link between retail trading and the correlation between cryptocurrencies and equities.

Next, we select the 3,000 US stocks with the most trading volume on the Swissquote platform and rank them by the trading activity of crypto traders. We divide this sample of stocks into quintiles. We look at the relationship between retail crypto trading volumes and correlation with Bitcoin for each quintile. We find that in periods with intense crypto trading activity, stocks tend to be more correlated with Bitcoin. Furthermore, this effect is significantly stronger for stocks preferred by crypto investors. Unsurprisingly, crypto investors tend to prefer tech and growth stocks. The fact that Bitcoin correlates more with the Nasdaq than with the S&P 500 is perfectly consistent with our proposed mechanism.

The extreme volatility of cryptocurrencies and their frequent crashes did not discourage many institutional investors from entering cryptocurrency markets. For instance, Goldman Sachs is considering acquiring the assets of the failed crypto-lending firm Celsius, and Fidelity introduced cryptocurrencies in the investable universe of its 401(k)s. The mechanism we highlight in our paper poses serious questions for banks and policymakers trying to understand the risks associated with widespread crypto adoption. Furthermore, this mechanism sheds light on the recent cryptocurrency crash, showing a plausible reason why tightening monetary policy translated into plummeting crypto prices. While the impact of retail investors on the stock market is limited, their impact on cryptocurrency markets is much more significant. In the absence of a clear fundamental value, swings in investors’ mood are often the driver of prices, and one could consider Bitcoin price as a noisy measure of retail investors’ sentiment.

Antoine Didisheim is a PhD candidate at the Swiss Finance Institute and HEC, University of Lausanne.

Luciano Somoza is a PhD candidate at the Swiss Finance Institute and HEC, University of Lausanne.

This post is adapted from the paper, “The End of the Crypto-Diversification Myth,” available on SSRN.

The views expressed in this post are those of the author and do not represent the views of the Global Financial Markets Center or Duke Law.