With the global push toward sustainable investment, investors are concerned about whether the cost of investing green will result in lower portfolio returns in the long term. Are there win-win strategies where green investments can generate high returns alongside positive environmental impact?

Our new paper, funded by the National Pension Hub at the Global Risk Institute, shows how Canadian pension funds have developed a win-win scenario through the atypical strategy of investing in green urban development. This strategy retrofits existing properties and develops new properties that meet the Leadership in Energy and Environmental Design (LEED) standards. Our research results show that large Canadian pension funds, which manage more than USD 50 billion of assets, have earned high real estate portfolio returns over the past two decades while driving the green development in major city centers.

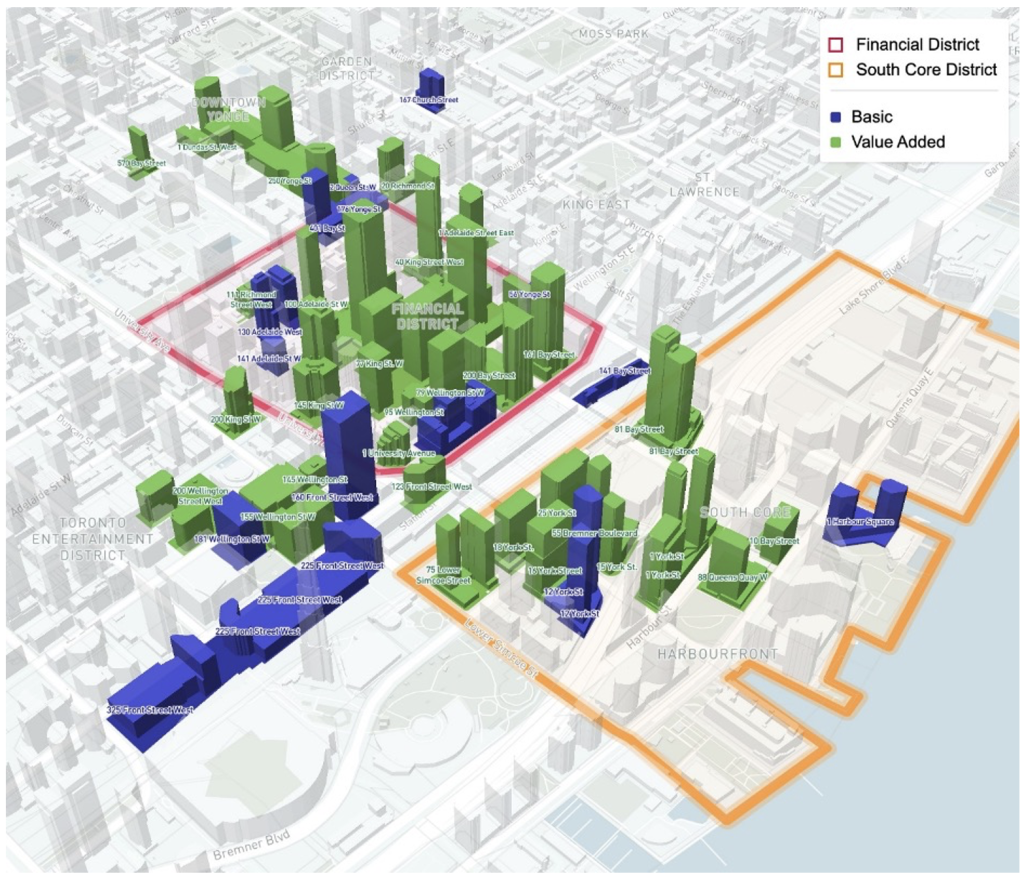

Take the case of Toronto. As Canada’s largest city and home to 5 head offices of the 9 largest Canadian pension funds, Toronto is a good case study to show the scope of green urban development by the funds. The map below illustrates Toronto’s financial district (red border) and the emerging South Core district (orange border). All the buildings colored green and blue are directly owned by the big 9 pension funds (AIMCo, BCI, CDPQ, CPPIB, HOOPP, IMCO, OMERS, OTPP, and PSP). The green indicates those properties that have obtained LEED certification under pension fund direct ownership.

The results are impressive. Virtually all of Toronto’s financial district buildings have been owned or are owned and greened by the major Canadian pension funds. The emerging South Core district is also being extensively developed by these funds through greenfield ventures. Not only this, but 17 of the 26 Toronto buildings that have obtained LEED Platinum—the highest level of LEED certification—have done so under pension fund ownership. We find similar patterns in Montreal and Vancouver.

Canadian pension funds investing in green urban development are unique in the global pension industry. Data from the Preqin database on hundreds of real estate deals made by large Canadian and non-Canadian funds reveal that, while large Canadian pension funds manage just 6% of global pension assets, they are responsible for 60% of the total value of direct real estate deals involving a pension fund. And, within their extensive scope of real estate investment, large Canadian funds complete LEED projects on 27% of their portfolio of direct acquisitions. By comparison, large non-Canadian funds complete LEED projects for only 14% of their portfolio. This gap only increases once we focus on office properties where LEED certification is most common.

Following this pattern, our analysis of the composition of the Canadian funds’ real estate portfolios shows that one large Canadian pension fund is equivalent to 10 non-Canadian funds of the same size in this market. Data on 241 funds in 8 countries from the CEM Benchmarking database (a global benchmarking company based in Toronto) shows that, on average, large Canadian funds invest significantly more in real estate (14% of AUM) than their peers (8.5% of AUM). The data also reveals that on average, large Canadian pension funds invest 81% of their real estate portfolio directly, whereas non-Canadian funds of the same size only invest 16% of their real estate portfolio directly. Direct real estate investments therefore make up 12% of the AUM of large Canadian pension funds (0.14 X 0.81 = 0.12) but only 1.2% of the AUM of large non-Canadian pension funds.

For Canadian pension funds, green urban development has become a win-win strategy for high returns on green investments. This has been made clear from our research on the annual return data of the funds’ real estate portfolios from the CEM Benchmarking database, where we applied a careful benchmarking methodology across funds. For each fund, we calculate the net value added (NVA) of its real estate portfolio in relation to its benchmark (net of fees) from 2005 to 2019.

The data shows that portfolios of large Canadian pension funds with a high proportion of direct real estate investments outperform their benchmarks. On average, large Canadian pension funds that directly manage more than 50% of their real estate AUM generated a NVA of 148 basis points and an average annual return of 9.7% between 2005 and 2019. By comparison, the average NVA was negative 215 basis points for non-Canadian funds. The performance of large Canadian pension funds confirms that the green urban development strategy creates financial value net of fees.

Green urban development is an impact investment strategy that departs from the well-known forms of pension fund activism, in that it is a strategy focused on project execution in private value-add real estate. Canadian funds do not share the ownership of projects with many investors in order to mitigate agency conflicts that arise when ownership is fragmented. Typical conflicts include expropriation or inefficient use of funds by managers when investors have limited ability to control the firm’s assets. Other benefits of this impact strategy include direct communication between owners and managers, low fees due to the elimination of financial intermediaries, lower cost of project financing, and the ability to extract the full economic profit from the real estate ventures.

However, there are legitimate concerns about the legal and operational risks associated with the development and management of real assets. There are also liquidity risks related to the long-term nature of development projects, and risks that the real estate industry faces in emergencies such as the COVID-19 pandemic. All these risks need to be considered for the long-term health of these investments.

We look for how Canadian pension funds have tried to mitigate these risks and discuss several strategies that they have put in place.

First, the evidence suggests that Canadian pension funds restrict this model of impact management to a specific set of projects in real estate. These projects are well defined (i.e., construction of a downtown tower), can be replicated in multiple cities, and have a risk profile that naturally matches the long-term bond profile of the funds’ liabilities.

Second, the properties developed by Canadian pension funds are mostly limited to standard multi-use properties located in prime downtown locations of major cities with diversified industries. As such, these projects can be adapted to multiple economic scenarios.

Third, Canadian pension funds combine local green urban development with a globally diversified portfolio of real assets. We also find evidence that Canadian funds increasingly invest in network and data centers around major cities, as these tend to do well in extreme scenarios like the current pandemic where retail activity is severely curtailed.

Finally, the use of wholly-owned real estate operating subsidiaries provides a number of operational advantages such as experience in developing and managing projects, access to a large network of suppliers and retailers that lease the space, protection from legal risks, additional flexibility regarding employee compensation, and the reduction of agency issues.

Our study highlights a possible strategy for other pension funds to follow. Most institutional investors outsource the majority of their active investments to external portfolio managers and incur large fees that often offset the active gains on the portfolio. By implementing the green urban development strategy internally, pension funds are able to generate long-term value for pensioners while contributing to sustainable urban development.

Alexander D. Beath is a Senior Research Analyst at CEM Benchmarking Inc.

Sebastien Betermier is an Associate Professor of Finance at the Desautels Faculty of Management at McGill University.

Maaike Van Bragt is a Financial Analyst at CEM Benchmarking Inc.

Yuedan Liu is an Advisor, CIO Strategy and Governance, at PSP Investments

Quentin Spehner is an Analyst at CEM Benchmarking Inc.