Seeking “strategic alternatives” is industry jargon for considering a potential sale or merger. During this process, the company gauges interest from potential acquirers. From 1990 to 2018, there were more than 1,200 announcements made by public companies revealing that they were reviewing strategic alternatives (examples here and here). Before deciding whether to disclose this information voluntarily, via a press release or SEC disclosure, executives or directors may ask: what are the costs and benefits of making the strategic alternatives process publicly known? Because an evaluation of strategic alternatives does not constitute a mandatory disclosure, the other option is to keep the process undisclosed until a deal, if any, materializes, and must then be announced.

In my paper, Economic Consequences of Announcing Strategic Alternatives, I analyze attributes of these corporate disclosures and their implications for the company’s operations, information environment, future mergers and acquisitions (M&A) sales process, and short-term and long-term share prices. This article explores the four key takeaways from this study.

Takeaway #1: Companies’ public announcements regarding strategic alternatives often contain common key phrases and details. These announcements generate 5.4% stock returns on average (measured over a 3-day window) and lead to subsequent offers and completed sales 41% and 32% of the time. However, certain key phrases signal deviations from these “average” occurrences.

82% of the announcements analyzed mention the retention of financial and/or legal advisors, and may specifically name the firms. Investors react to such announcements with stock returns that are 4.4% higher.

65% of the announcements analyzed specifically mention the sale of the company as an alternative under consideration. Announcements that contain this specific alternative generate returns that are 3.4% higher and are associated with a greater probability of being acquired.

63% of the announcements analyzed state that the company is seeking strategic alternatives to maximize or enhance shareholder value. Investors react to announcements containing such phrases with returns that are 2.5% higher.

Other common features of companies’ announcements include: a direct quote from an executive, director, or other company spokesperson explaining why the company is seeking strategic alternatives; mentioning that the directors have formed a special committee to oversee the strategic alternatives process; bundling the announcement with an earnings report and earnings guidance; mentioning that an activist investor called for the company’s evaluation of strategic alternatives.

Takeaway #2: The benefits of publicly announcing the evaluation of strategic alternatives include heightened market attention from investors and a more robust M&A sales process, eventually leading to a greater probability of receiving an offer and consummating a transaction.

41% of strategic alternatives announcements are followed by an M&A offer within a year, representing an increased probability of about 34% over the baseline 7% probability of receiving an offer.

32% of strategic alternatives announcements are followed by a completed transaction within a year, representing an increased probability of about 27% over the baseline 5% probability of being sold.

The reason why strategic alternatives announcements lead to more successful M&A outcomes is because the news (public, in nature) reaches more market participants and potential suitors. The evidence in the study is consistent with this hypothesized reason: the announcement leads to increased downloads of the announcing company’s SEC filings, more M&A bids submitted for the company, a more diverse group of bidders (i.e., from different industries than the announcing company’s), and the timelier receipt of an offer. All these characteristics indicate a more robust M&A sales process, where all potential bidders are made aware of the company putting itself up for sale, so that the most ideal suitor and offer emerges in a timely fashion.

Takeaway #3: The costs of a public strategic alternatives process include increased disruption to the core business operations and seeding a negative public perception that alienates relationships with stakeholders such as customers and employees.

Financial performance—as measured by return on assets, operating income, and their seasonal changes—is abnormally lower in the first full fiscal quarter following the announcement of strategic alternatives. This occurs because managing a strategic alternatives process is a major distraction for executives and managers from running the business; since the public announcement generates greater attention and more inquiries, the distraction and disruption is greater as well.

In addition, the study finds that sales revenue, its seasonal change, employee headcount, and its annual change are abnormally lower following the announcement of strategic alternatives. This suggests that the company’s stakeholders see an announcement of strategic alternatives as a public admission of business problems. Companies seek strategic alternatives when the trajectory of the current stand-alone business strategy is troublesome—the company is essentially admitting that greater shareholder value could be achieved by selling the business than from continuing to run it. If a company makes its strategic alternatives evaluation publicly known, customers are likely to disengage with a company whose product offerings and customer service they perceive to be on the decline or about to cease altogether given a perceived future change in control. Similarly, employees feel that a potential change in control threatens their job security and employment conditions and thus are less focused and productive. In some cases, they may even leave the company.

Takeaway #4: Companies may conduct a cost-benefit analysis of making the public disclosure by looking at the impact of the announcement’s costs and benefits on long-term shareholder value.

For the sample as a whole, the negative effects of the announcement (e.g., worse business operations in takeaway #3 above) hinder one-year returns by about −19%.[1] However, if the company announces and is successful at getting acquired, the negative valuation consequence is offset by the valuation benefit from disclosure (e.g., increased probability of getting acquired and receiving a higher takeover premium from the ideal acquirer in takeaway #2 above). Thus, the acquired company nets about 9% higher shareholder returns from making the public announcement. However, most announcing companies are not eventually acquired. Therefore, the typical company is more likely to suffer the valuation consequences without being able to capture the benefit. Hence, the unconditional average long-run valuation effect from announcing is about −5%.

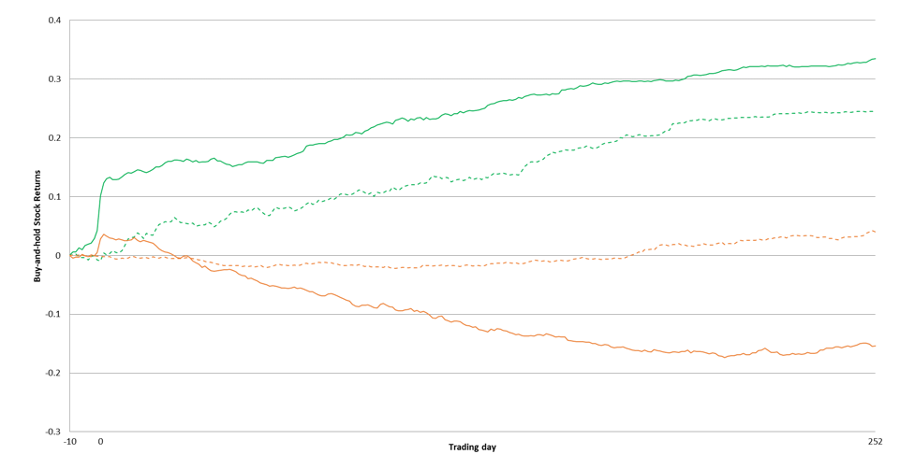

Effect of the announcement on shareholder value

Figure (a):

Effect of the announcement on shareholder value — partitioned by subsequent takeover status

Figure (b):

Effect of the public announcement on shareholder value. Stock returns are measured over trading days [-10, +252] relative to the announcement, and the market return has been subtracted from all lines. Figure (a): The solid line depicts the mean stock returns of companies that announced they are seeking strategic alternatives. The dashed line represents the counterfactual returns estimated using peer firms with similar characteristics, but that did not announce. Figure (b): The stock returns are separately presented for the subset of firms that are subsequently acquired, in green, or are not acquired, in orange. As in figure (a), the solid lines depict the mean returns of announcing companies, and the dashed lines represent the counterfactual returns estimated from non-announcing peer firms.

While the study presents quantitative estimates of the valuation consequences of disclosure for the sample as a whole, individual companies should conduct assessments of their unique costs and benefits from publicly disclosing their strategic alternatives process. Considerations of the announcement’s costs involve estimating the destruction of shareholder value from disrupting business operations and alienating stakeholders such as employees and customers. The resulting dysfunction may be less severe for a company that can shield the core business operations from the strategic alternatives evaluation process (e.g., segregating key employees’ duties) and can effectively manage communications with key stakeholders about the company’s continued dedication to its existing products and customer service (for customers) and corporate organization and culture (for employees). Considerations of the disclosure’s benefits involve an honest assessment of the increased probability of the transaction as a result of publicizing the strategic alternatives evaluation, and of the increased takeover premium that could be captured by shareholders from the ideal acquirer. A company that operates in a well-known industry with fewer players may be able to contact all potential buyers without a public announcement, and in this case, the benefit of disclosure may be limited.

Conclusion

As the four takeaways above described, this study documents various costs and benefits to a company of publicly announcing that it is seeking a potential sale or merger (“strategic alternatives”) and the impact of announcing on short-term and long-term shareholder value. A firm’s decision to announce causes costly disruptions to the business operations and stakeholder relationships which erode firm value. On the other hand, the announcement improves market attention to the company which may increase takeover-related gains to shareholders (if the company is subsequently acquired) and offset the costs.

The findings of this research are important because they provide 1) evidence of various channels between a disclosure choice and shareholder value; 2) separate, offsetting estimates of the disclosure’s costs and benefits affecting firm value; and 3) key considerations to investors and company decision makers who would face the consequences of this disclosure decision.

Jenny Zha Giedt is an Assistant Professor at the George Washington University School of Business.

This post is adapted from her paper, “Economic Consequences of Announcing Strategic Alternatives”, available on SSRN.

[1] For simplicity, the percentages presented in this article are point estimates, whereas the study presents a range of magnitudes estimated from various model specifications.

Hello Jenny!

It’s always a question to be – or not to be. Even when it comes to M&A, there’s no definitive answer about how a given company should play the game. It’s good to see that you’ve disclosed the advantages of disclosing the process of seeking strategic alternatives, as well as its downsides. In the end of the day, one should make the right decision, and being right does not always mean “easy”.

Thanks for your comment Marina. You’re absolutely correct in that the cost-benefit analysis of whether/how much to disclose is going to vary based on the individual company’s unique circumstances.

There are many considerations involved, and a few questions strategic leadership can ask themselves are:

1. Are there many potential acquirers from various industries that may emerge following a public announcement of my company’s search for strategic alternatives, or can I rely on my financial advisor to identify and contact substantially all of the potential suitors?

2. How confident am I in the company culture that employees will not be disrupted or tempted to jump ship if they are aware that the company is evaluating strategic alternatives?

3. Are customers likely to transfer to a competitor’s services if they hear that my company is seeking a merger, or are they unperturbed by a potential transaction?

Is a company CEO bound by silence during the SR process? What can he/she say while it is ongoing?