When the Covid-19 outbreak became a national emergency in the United States, the Federal Reserve, having learned the lessons from the last crisis, was quick and bold in reacting. In only nine days, from March 15 to March 23, the Fed cut its target for the federal funds rate, provided forward guidance, intervened in markets by purchasing Treasury and mortgage-backed securities, expanded the scope of its repo operations, encouraged the use of the discount window and intraday credit, offered dollar liquidity to foreign central banks, relaxed regulatory requirements, and announced the establishment of six emergency lending facilities invoking Section 13(3) of the Federal Reserve Act (FRA).[1]

On March 27, President Trump signed into law the Coronavirus Aid, Relief, and Economic Security Act, or the CARES Act,[2] a piece of legislation that, unlike the Troubled Asset Relief Program (TARP) during the global financial crisis (GFC), was expeditiously passed by Congress. The CARES Act appropriated over $2 trillion to alleviate the negative economic effects of the pandemic, with at least $454 billion allocated to support Fed programs.[3] The appropriation provided funding for the Treasury’s Exchange Stabilization Fund (ESF), to cover losses from the Fed’s emergency lending facilities.[4]

Considering that Section 13(3) of the FRA,[5] as amended by the Dodd-Frank Act, already granted the Fed authority to act as a lender of last resort in crises, what additional legal powers did the CARES Act give to the Fed when it comes to the emergency lending facilities?

What was already there

Section 13(3) of the FRA authorizes the Fed (more specifically, the Board of Governors of the Federal Reserve System) to offer liquidity to non-financial institutions in “unusual and exigent circumstances.” The market turmoil caused by the pandemic and the “dash for cash” that took place in financial markets last March left no doubt that we were facing unusual and exigent circumstances.

The purpose of the FRA regarding emergency lending is to preserve financial stability by providing liquidity. According to Section 13(3)(B)(i), the Board can authorize a Federal reserve bank to provide emergency lending to any participant in a program or facility with broad-based eligibility “for the purpose of providing liquidity to the financial system.”

This legal authority implies that the Fed has the power to create high-powered money and flush the markets with liquidity in case of panic, thereby allowing the Fed to act as lender of last resort. For that reason, true lender-of-last-resort facilities dispense with any immediate backstop by the fiscal authority, even when the law requires the Treasury Secretary’s consent for the central bank to act, as does Section 13(3) of the FRA since its amendment by the Dodd-Frank Act in 2010.

In the Fed’s response to the Covid-19 crisis, the emergency facilities that were created to provide liquidity for non-bank financial firms—the Primary Dealer Credit Facility (PDCF), the Commercial Paper Funding Facility (CPFF), the Money Market Mutual Fund Liquidity Facility (MMLF), and the Term Asset-Backed Securities Loan Facility (TALF)—are all traditional lender-of-last-resort facilities, or “liquidity facilities.” This means that they could have been structured under Section 13(3) of the FRA without any equity coming from the Treasury, although the PDCF is the only one among them that did not end up having this backstop.

What came to be

The CARES Act went beyond Section 13(3) of the FRA by authorizing the Fed to provide “liquidity to the financial system that supports lending to eligible business, States, or municipalities” (Section 4003(b)(4)).[6] The purpose of the programs and facilities created under the CARES Act is not to provide liquidity to the financial system as an end in itself, but to use the financial system as a vehicle to provide liquidity to businesses, States, and municipalities suffering losses incurred as a result of the pandemic.[7]

This additional purpose is compatible with the nature of the present crisis—the United States is now facing the economic consequences of a public health crisis, not a crisis born in the financial system, as was the GFC (banks are now healthier than in 2007-2009, in great part due to Dodd Frank’s strict guidelines).

The CARES Act authorizes the Treasury Secretary to use at least $454 billion to make loans, loan guarantees, and other investments in the programs and facilities established by the Board.[8] The resources for that correspond to the amounts appropriated to the ESF, a stabilization fund that belongs to the Department of Treasury.[9] Moreover, the Secretary of Treasury can attach terms and conditions to the loan, loan guarantee, or investment as he determines appropriate.[10]

The combination of these factors (the additional purpose, the financial participation of the Treasury, and its wide discretion in setting terms and conditions) reveals that the Fed programs and facilities authorized by the CARES Act are meant as a vehicle for the Treasury to implement fiscal policy, in the form of credit policy, and not an expansion of the Fed’s legal mandate as lender of last resort. In this sense, the CARES Act has not expanded the Fed’s monetary-policy mandate. Rather, it has created a new role for the Fed—that of conduit for fiscal-policy implementation through the financial system.

This new role has not turned the Fed into an investment authority. According to the CARES Act, the Treasury has great leeway in picking winners and losers in these programs and facilities. It has, nevertheless, deferred the conception and administration of these programs and facilities completely to the Fed, who has thus received all criticism related to undeserved favors, too stringent rules, and conflicts of interest.

Why it matters

When used as a vehicle for fiscal policy implementation, the Fed programs and facilities will have the characteristics described in Section 4003 of the CARES Act and cannot risk losses that go beyond the amounts invested, lent, or guaranteed by the Treasury via the ESF.

However, if such programs and facilities have the final goal of providing liquidity to the financial system, losses do not have to be immediately backstopped by the Treasury. In a true Section 13(3) emergency program or facility, Treasury investment is not necessary, as the Fed can act as lender of last resort.

In both cases, taxpayers may take losses because the Fed’s balance sheet losses are eventually transferred to the Treasury. And both Section 13(3) of the FRA and Section 4003 of the CARES Act require the Fed to demand sufficient guarantees to protect taxpayers from losses.[11]

The difference is that, under the CARES Act, the programs and facilities are prohibited from accepting losses greater than the Treasury’s investments, loans, and guarantees, which in turn are limited to an amount that could go from $454 billion to $500 billion. That is the criterion the Fed would have to adopt when deciding whether the collateral secures the operations to “its satisfaction.”

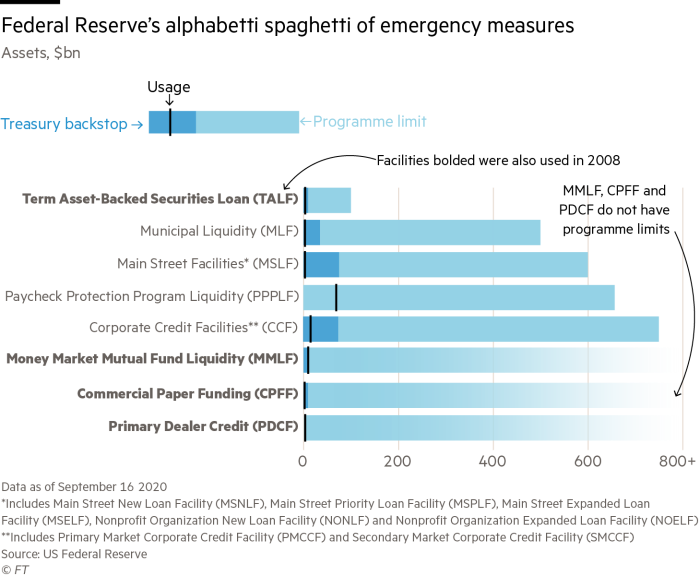

The prohibition may not be an issue in practice, since the Congressional Budget Office (CBO) has estimated that the additional lending under the CARES Act regarding the Fed programs and facilities will not have budgetary effects, considering that the income and costs anticipated for the assistance will roughly offset each other. Accordingly, as of September 16, not even half of the equity provided by the Treasury had been used (see Figure 1, below). And only $195 billion (of the $454 billion appropriated by the CARES Act) has been effectively committed to cover losses in the Fed emergency facilities and programs.

Figure 1

In Section 13(3) emergency lending programs and facilities, on the other hand, the Board gets to decide the level of losses acceptable in the operation of the programs and facilities, guided by the objective of providing liquidity to the financial system, but not limited to a specific figure, as with the CARES Act.

The FRA does impose further boundaries to the Fed’s assistance, such as (1) the assistance must be “secured to the satisfaction of the Federal Reserve bank;” (2) the Federal Reserve bank shall obtain evidence that the participant is “unable to secure adequate credit accommodations from other banking institutions”; (3) the security for the loans must be sufficient to protect taxpayers from losses; and (4) insolvent entities must be prohibited from borrowing.

These constraints must also be observed in the CARES Act assistance, as determined by Section 4003(c)(3)(B), which expressly mentions the FRA requirements “relating to loan collateralization, taxpayer protection, and borrower solvency.”

Additionally, it is not clear that the types of operations allowed for FRA emergency programs and facilities coincide with those authorized by the CARES Act. Under Section 13(3)(A) of the FRA, the Board can authorize any Federal reserve bank to discount, for any participant, notes, drafts, and bills of exchange when such notes, drafts, and bills of exchange are indorsed or secured to the satisfaction of the Federal Reserve bank. The CARES Act permits a broader array of operations, all listed in Section 4003(b)(4): purchasing obligations or other interests directly from issuers or in the secondary market or otherwise, and making loans, including loans or other advances secured by collateral.

For the sake of assessing the achievement of goals stated in each of the two statutory provisions, the economic effect seems to be always the same—providing liquidity to the participants in programs and facilities. More than that, the reference to “loans” in different passages of Section 13(3) of the FRA,[12] notably the requirement that the Board provides a report concerning “any loan or other financial assistance,”[13] confirms that the expression “discounting notes, drafts, and bills of exchange” can be interpreted broadly.

However, the establishment of Special Purpose Vehicles (SPV) as part of the design of the programs and facilities now, and in 2008, indicates that the operations—discounting securities, purchasing obligations or other interests, and making loans—do have differences. Using the SPV structure allows the Fed to keep directly on its balance sheet only the loans it makes to the SPV; the SPV can then do other types of transactions, such as asset purchases. That avoids questions around the types of operations permitted to the Fed under Section 13(3) and the counterparties with which it can do each kind of operation. The CARES Act, in turn, does not raise the same kind of concern, given the express authorization to purchase obligations or other interests.[14]

“Whatever it takes,” within the legal mandate

It is not surprising that the Board has referred to both statutes—the FRA and the CARES Act—as the legal basis for the emergency programs and facilities announced during the pandemic. The CARES Act does not grant the 10:1 leverage power the Board has assigned to those programs and facilities, and that seemed crucial to convince markets that the Fed, too, will do “whatever it takes” to save the economy. It is Section 13(3) of the FRA that gives the Fed this leverage power. And as Mario Draghi did in his famous 2012 speech supporting the euro,[15] Fed Chairman Jerome Powell has repeatedly made clear that the central bank is acting within its legal mandate. Apparently, the Fed’s objective was achieved—the modest usage of the facilities signals that their mere announcement has boosted confidence in financial markets (see Figure 2), which then provided much of the missing credit and liquidity.

Figure 2

The miracle of money creation operated by the Fed will not come for free—the Fed pays interest on the new bank reserves that are created with the emergency lending and other policies, such as quantitative easing. That is the “lever-up fallacy” George Selgin calls attention to, reminding us that the Fed is part of the government and, as such, its results, either positive or negative, are eventually remitted to the Treasury.

The Fed and the United States, as stewards of the global reserve currency, can probably afford that fiscal burden, either by the Treasury issuing debt, or indirectly through the Fed printing money. This is particularly true in a scenario of low interest rates, which also means low costs for financing government debt. In any case, the legislative decision to backstop Fed lending with appropriated funds transferred by the Treasury might well have been a political move designed to avoid controversy around the Fed providing credit to the real economy. But it was not a decision without legal implications.

The legal authority that the CARES Act gives to the Fed is not merely an extension of the Section 13(3) traditional lender of last resort role—as seen, each statute assigns a fundamentally different mission to the Fed. Understanding this difference and teasing out how the Fed’s recent actions fit into its legal mandate is instrumental in holding the central bank accountable and preserving its credibility, especially in light of the distributional effects of the quasi-fiscal policies implemented by the Fed under the CARES Act.

Juliana B. Bolzani is a lawyer at the Central Bank of Brazil and an SJD student at Duke Law School. The views and opinions expressed here are hers and do not reflect the position or policy of any of the institutions with which she is affiliated. For comments, please contact juliana.bolzani@duke.edu.

—

[1] These are the emergency lending facilities initially announced by the Fed: Commercial Paper Funding Facility (CPFF), Primary Dealer Credit Facility (PDCF), Money Market Mutual Fund Liquidity Facility (MMLF), Primary Market Corporate Credit Facility (PMCCF), Secondary Market Corporate Credit Facility (SMCCF), and Term Asset-Backed Securities Loan Facility (TALF). Two additional facilities and one umbrella program were announced by the Fed on April 9: Paycheck Protection Program Liquidity Facility (PPPLF), Municipal Liquidity Facility, and Main Street Lending Program. The Main Street Lending Program includes five facilities: Main Street New Loan Facility (MSNLF), Main Street Expanded Loan Facility (MSELF), Main Street Priority Loan Facility (MSPLF), Nonprofit Organization New Loan Facility (NONLF), and Nonprofit Organization Expanded Loan Facility (NOELF).

[2] P.L. 116-136.

[3] On top of the $454 billion, Section 4003(b)(4) of the CARES Act states that the Fed’s programs and facilities would also have available the unused portion of the $46 billion appropriated for loans and loans guarantees to passenger air carriers, air cargo carriers, and businesses important to maintain national security.

[4] Section 4027 of the CARES Act.

[5] 12 U.S.C. § 343(3).

[6] See also Section 4003(c)(3)(E), using the same language.

[7] See Section 4003(a), which describes the general goal of the CARES Act emergency relief.

[8] See Section 4003(a), Section 4003(b)(4), Section 4003(c)(1)(A), Section 4003(c)(3)(A)(ii), Section 4003(c)(3)(C), and Section 4003(c)(3)(D).

[9] 31 U.S.C. § 5302.

[10] Section 4003(c)(1)(A).

[11] See Section 13(3)(B)(i) of the FRA and Section 4003(c)(3)(B) of the CARES Act, the latter expressly extending the requirements of Section 13(3) of the FRA to the CARES Act programs and facilities, “including requirements relating to loan collateralization, taxpayer protection, and borrower solvency (…)”

[12] Section 13(3)(A)(i): “emergency loans”; “loan executed by a Federal reserve bank”; “loan is secured satisfactorily”; Section 13(3)(E): “loan under this paragraph”; “while such loan is outstanding”; “net loss on the loan”.

[13] Section 13(3)(C).

[14] Section 4003(b)(4).

[15] In the speech, Draghi explained that “to the extent that the size of these sovereign premia [the premia that were being charged on sovereign states borrowings] hampers the functioning of the monetary policy transmission channel, they come within our mandate.”