This post is the fourth in a series that highlights various elements of a new online course titled “FinTech Law and Policy.” The course is available to all on the Coursera platform (it can be audited for free) and covers the key legal and regulatory issues confronting the FinTech industry today. You can view all previous posts in the series here.

Why have we yet to see some version of Uber or Airbnb disrupt the banking industry? Before you answer that question, think about how these two companies got to where they’re at today. When Uber wanted to operate in New York City, did they go to the New York City taxi and limousine commission and ask for permission? Same for Airbnb, did they seek a hotel license to operate in each city? Of course not! These two companies identified a market need, built a product to meet this need, and then released it to the public. Consumers flocked to these products because they were far superior to anything else out there, and government agencies around the world were left with little choice but to accommodate these new products, lest they provoke their citizenry.

So again, why hasn’t something like Uber or Airbnb happened in the banking industry? Is it because most of us are generally satisfied with our current bank and therefore there is no market need? Given the lack of consumer trust in the financial industry, especially since the financial crisis, I would say the answer is no. The real reason is that the banking industry is fundamentally different from any other industry because you’re dealing with people’s money. Along with that, comes a high degree of regulation by multiple regulatory agencies at the federal and state level.

In essence, the Uber and Airbnb mentality of “it is better to ask for forgiveness than permission,” simply does not work in finance. This does not mean that some FinTechs haven’t aspired to be the Uber or Airbnb of finance. After all, many of the technologists at the forefront of the FinTech boom are cut from the same cloth as those that ushered in the sharing economy, adhering to the Silicon Valley mantra of “move fast and break things.” These people are risk takers, who spend little time thinking about, and have little regard for, regulations. Some of these early FinTech firms sought to deploy their products and services before regulators had a chance to understand exactly how the product worked and how it fit into the existing regulatory regime. This method does have its advantages, mainly that consumers might actually enjoy the product and benefit from its use. This puts pressure on the regulators not to intervene too aggressively. But of course, this strategy also carries significant risk – the biggest being that one or more regulatory agencies shuts the company down for good.

As time has gone on and regulatory agencies have increasingly exerted their authority, FinTech innovators have come to understand that disrupting any aspect of finance is no easy task. This reality has led to a shift in mentality within the FinTech industry, from disruption to partnership. Now, the stated goal of many new FinTech firms is to partner with, or be acquired by, a traditional financial institution. We can see this fact reflected in figure 1.1 below, which shows how venture capital funds are cashing out of their investments in FinTech companies. We can see clearly that the most common way for venture capital funds to exit their FinTech investments is through a strategic acquisition, meaning that the FinTech company they’ve invested in was purchased by a financial institution or possibly even a larger FinTech company. The number of strategic acquisitions has been steadily increasing and reached a peak in 2017 with fifty-nine.

Figure 1.1

Even with this growth in strategic acquisitions, it is not easy for a FinTech to be purchased by, or even partner with, a traditional financial institution. In a 2017 survey, global consulting firm PwC asked FinTech companies and financial institutions what the biggest challenges were when it came to working with one another.[i] For financial institutions, the biggest challenge in working with FinTech companies is IT security. This makes sense given how tightly regulated traditional financial institutions are and the expectation of regulators and customers alike that the institution appropriately safeguard customer data. For financial institutions, a major data breach could seriously threaten the ongoing viability of the firm. When FinTech companies were asked what challenges they faced in working with financial institutions, the most common answer given was “differences in management and culture.” This answer also makes sense given the more freewheeling culture within tech startups, which contrasts sharply with the button down, hierarchical structure of many financial institutions.

Banks are also going to be more naturally cautious when it comes to working with FinTech firms because they are liable for risks posed by third parties. This means that banks will spend significant amounts of time conducting due diligence on the practices and controls in place at FinTech firms seeking to partner with them in order to prevent unnecessary compliance or operational risks. Small banks with fewer resources to dedicate to due diligence may be unwilling to risk partnering with FinTech firms. Bank due diligence can lead to lengthy delays in establishing partnerships, which can put FinTech firms at risk of going out of business if they do not have sufficient funding on-hand and are unable to access new customers on their own.

Despite these challenges, a bank-FinTech partnership can be mutually beneficial. For banks, partnering with a FinTech can allow them to offer greater consumer choice and a better customer experience, along with potentially lowering costs through the more efficient use of new technologies. For FinTechs, partnering with a bank provides access to customers, financial resources, and regulatory expertise.

Trends in FinTech Investment

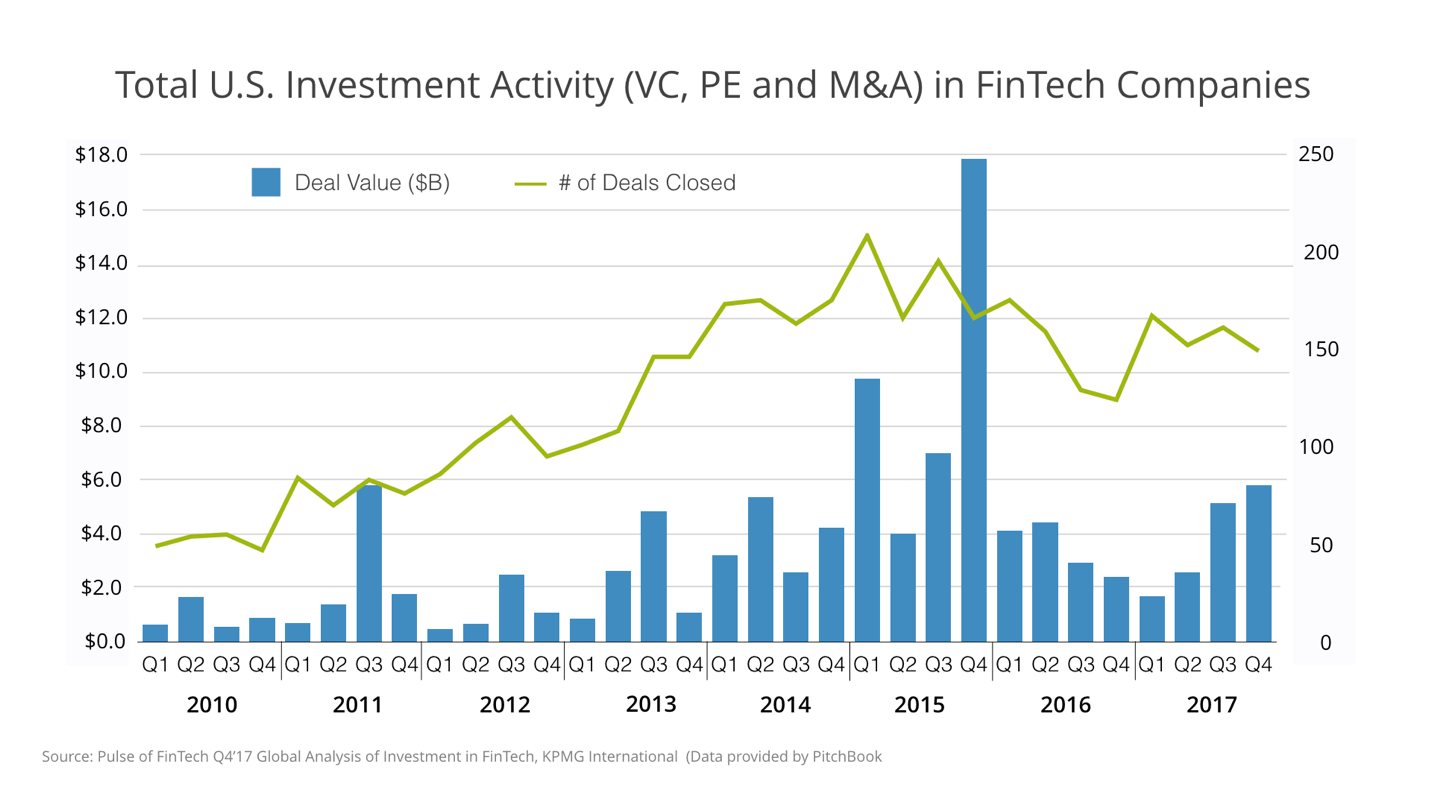

Figure 1.2 shows the growth in global investment activity in FinTech companies by quarter, dating back to 2010. This includes investment from venture capital funds, private equity funds, and investment through mergers and acquisitions. There was steady growth in the years immediately after the financial crisis and this growth peaked in the fourth quarter of 2015 with $24.8 billion dollars in new investment. FinTech investment activity has cooled off significantly since then in terms of deal value but the number of new deals closing every quarter has remained relatively stable, with over 300 new deals closing every quarter since the beginning of 2014. Figure 1.3 shows that US investment activity in FinTech companies has followed a similar trend as global activity, with the value of new deals peaking in the fourth quarter of 2015.

Figure 1.2

Figure 1.3

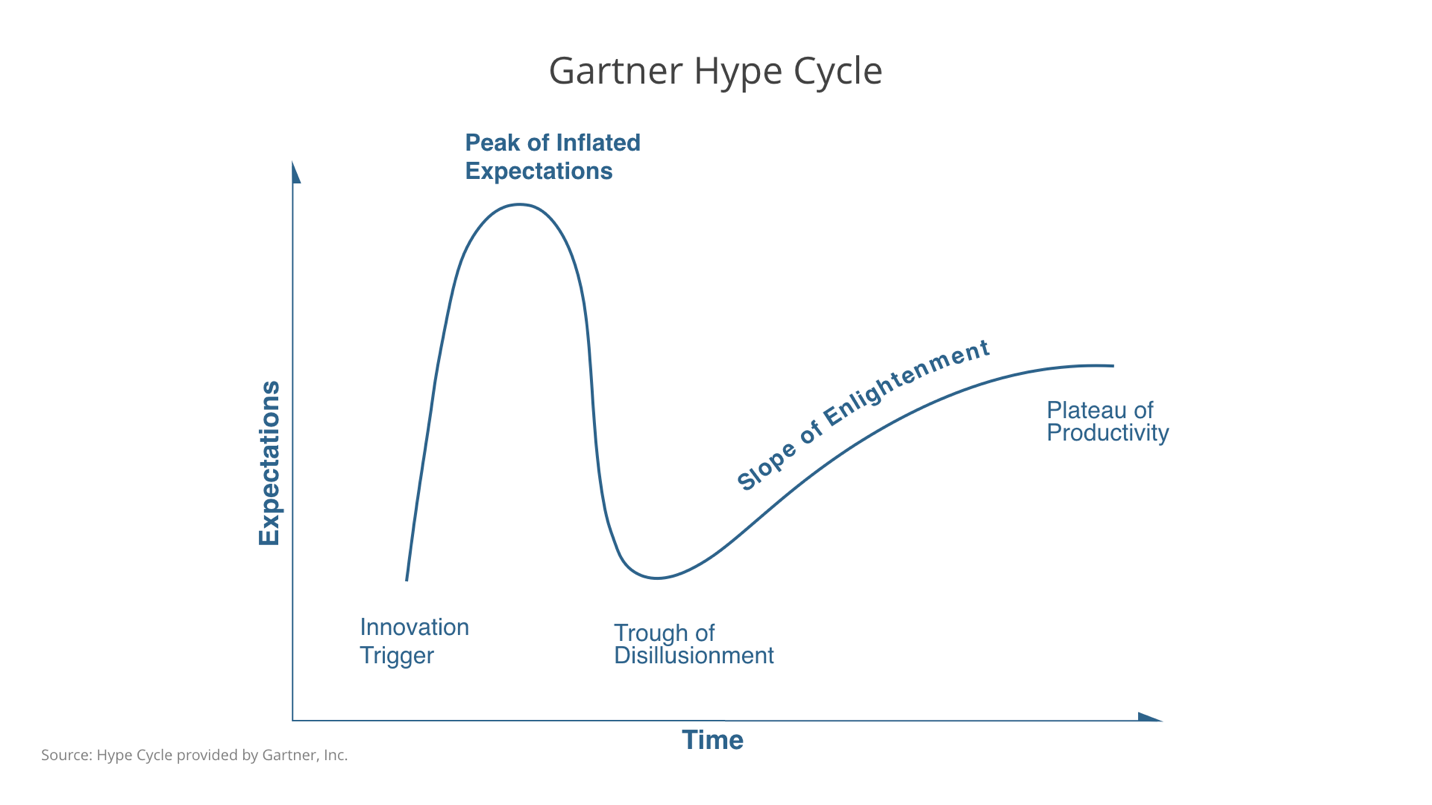

The fact that the value of new investments flowing into FinTech companies has come down considerably since 2015 while the overall number of new deals has remained stable reflects a decrease in FinTech company valuations that corresponds to the shift in industry mentality from disruption to partnership. In the FinTech industry’s early years, after the financial crisis, there was considerable optimism that FinTech would transform financial services the way Amazon transformed retail or Uber transformed transportation. This optimism was aided by buzzwords like blockchain, which was promoted as a revolutionary new technology that would fundamentally alter the finance industry and eventually the entire economy, but which few people actually understood. This hype and optimism led to a flood of new money pouring into the FinTech industry as we just saw. But when many of these freshly funded FinTech companies failed to deliver the hoped for results, investor sentiment returned to more realistic levels and new investment activity cooled off. This has led many to argue that the FinTech industry is going through the hype cycle, a term coined by the consulting firm Gartner, to reflect the maturity and adoption of new technologies. The hype cycle [see figure 1.4] is a visual representation of the fact that we tend to overestimate the effect of a new technology in the short run and underestimate the effect in the long run. Thus, according to hype cycle terminology, 2015 may have been the peak of inflated expectations for the FinTech industry. While it is hard to say with certainty where we’re currently at in the hype cycle, it is fair to assume that in the long-run, FinTech will prove to be a disruptive force in all aspects of finance.

Figure 1.4

[i] https://www.pwc.com/gx/en/industries/financial-services/assets/pwc-global-fintech-report-2017.pdf

Great overview. Exactly same disruption is happening in Europe, now there is payment service directive 2 coming in few months that will push banks to open up their API’s to third parties. Also the whole financial market is moving more and more to platforms, while banks at least in Northern Europe are down scaling their branches and relying platforms to bring customers they need. More or less same, what happened with hotels and travel industry.

Great article!

Fintech has for sure really been pushing up the API’s. Good content!

Such a spot on article! Fintech is definitely moving forward from the disruptive phase and in the near future we’ll see many interesting developments.

For example in our country, in Finland we have a thriving fintech ecosystem already in place. Finland is the place with high research value embodied in many aspects, and we can be viewed as a pioneer in mobile industry and alternative payments.

Exactly. It may seem that the general economic trend in Europe is migrating toward platforms rather than banks, but that’s far from reality today. Traditionally, banks have been concerned with maintaining physical contact with customers and servicing them in person. In this article, the author explains how that has shifted.

Great article. Fintech is definitely moving forward to interesting phase!

Great content! Fin tech is definitely one of those areas were we are going to see lot happening in the up coming years. So it’s always interesting to read about the state of the art in the industry, especially when it’s laid out this clearly!

Insightful analysis! The stark differences in regulation, risk, and the sensitive nature of finances explain why we haven’t seen a direct Uber or Airbnb-like disruption in banking. The shift towards collaboration and partnership in FinTech makes sense given these complexities.

Insightful analysis indeed! The pronounced disparities in regulation, risk management, and the delicate realm of financial services elucidate why there hasn’t been a straightforward disruption akin to Uber or Airbnb within the banking sector. Given these intricacies, the move towards fostering collaboration and partnerships in FinTech is a logical progression.

Sadly, I’m fairly certain that today, these trends have started to turn upside down. When looking at recent trends on stock markets, it’s clear that investors have started to turn their backs to fintech companies, especially after many have been burned after they initially jumped on the fintech trend. I’ve also personally worked with a few fintech companies that initially had great success (around 2018-2022), after which they started quietly slowing down until today, they’re barely even afloat. We’ll see how things go, but while they disrupted things for a while, things have turned around now.

The fintech industry’s evolution from disruption to partnership is a fascinating journey that highlights the importance of innovation and collaboration in financial services. For those interested in exploring modern loan solutions and learning about the latest trends in the lending market, I recommend visiting Kiired Laenud. It offers insightful resources and tools to help consumers navigate the diverse loan options available today.

The shift from disruption to collaboration signals an evolution in the FinTech industry. Instead of overthrowing traditional banking, many FinTechs now aim to integrate or be acquired by established financial institutions. This isn’t necessarily a loss—it reflects a maturity in strategy and a recognition that meaningful change in finance requires cooperation, not rebellion.

So, while we may not see an “Uber for banking,” the marriage of FinTech innovation and traditional banking stability could bring the best of both worlds. Maybe disruption in finance doesn’t have to mean breaking things—maybe it’s about building better together.