The role of hedge funds in U.S. Treasury (UST) markets is thought to have increased in importance since the global financial crisis (GFC) as bank-affiliated broker-dealers ceded some of their traditional activities in UST market arbitrage and liquidity provision to non-bank financial institutions. While UST securities play a vital role in the global financial system, hedge funds’ impact on UST market functioning is not well understood because they are less regulated than traditional broker-dealers and provide few disclosures. When compared to other asset managers, hedge funds employ substantial leverage coupled with investment strategies that are illiquid. They also have distinct funding structures, the resilience of which is key to understanding how they operate during periods of financial market turmoil. Following the unprecedented volatility in Treasury markets in March 2020, there has been much debate in industry, policy, and academic circles about the role hedge funds played during this crisis and, more broadly, the financial stability implications of hedge fund UST market activities.

In our new working paper, Hedge Fund Treasury Trading and Funding Fragility: Evidence from the COVID-19 Crisis, we conduct an empirical study bringing together comprehensive regulatory data to give, for the first time, a granular view of how hedge funds face a systematic crisis in terms of their liquidity and leverage management. To better understand the March 2020 shock, we analyze changes to hedge fund UST long/short notional and duration exposures, bilateral repo borrowing, collateral and funding terms, cash buffers, portfolio liquidity, and leverage. Further, we harness hedge fund-creditor level counterparty credit exposure data to investigate the role of creditor constraints and funding supply shocks. The COVID-19 crisis provides a unique opportunity to examine the strengths and vulnerabilities of the current model of UST market intermediation in which hedge funds play an important role.

Our overarching question is: Did hedge fund activities provide liquidity to UST markets through the March 2020 dislocation? If not, why not? To probe deeper into the factors that may have constrained hedge fund arbitrage activity and liquidity provision, we consider two additional questions:

- What was the impact of external debt and equity financing constraints? Specifically, we analyze whether the regulatory constraints of creditors—particularly those of dealers that are subject to enhanced regulations as part of global systemically important banks (G-SIBs)—hindered the ability of hedge funds to obtain funding, thus exacerbating the liquidity shock in UST. On hedge fund equity, we examine investor outflows during the market turmoil and the differential impact of hedge fund share restrictions that place limits on redemptions.

- What was the impact of hedge fund-specific liquidity management considerations? These involve both meeting unexpected, immediate liquidity drains such as margin calls and reacting to anticipated future liquidity needs in a time of aggregate uncertainty.

Leading up to March 2020

In the period leading up to the March 2020 COVID-19 shock, we find that hedge fund UST exposures doubled from early 2018 to February 2020, reaching $1.4 trillion and $0.9 trillion in long and short notional exposure (see Figure 1), respectively, primarily driven by relative value arbitrage funds, which held close to $600 billion in long UST exposure in February 2020.

Figure 1: Evolution of hedge fund UST exposures, repo exposures, average monthly returns, and cash. The grey vertical bar highlights March 2020. The US Treasury Exposure and Repo Exposure subfigures are for all hedge funds in our sample; the Returns and Cash subfigures are for all UST-trading hedge funds. Source: KMPW.

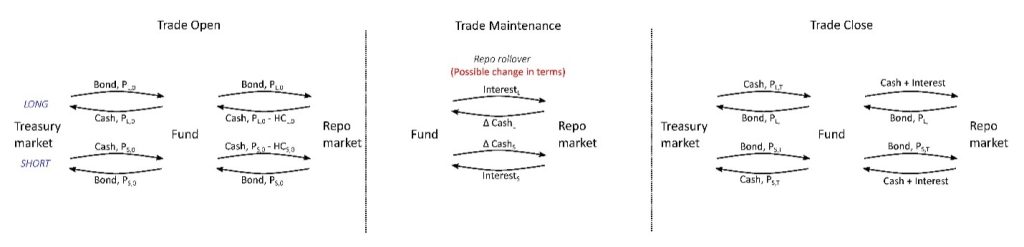

Long UST securities positions are primarily financed via repurchase agreements (repo borrowing), while short UST securities positions are primarily sourced through reverse repo (repo lending). Since 2018Q2, there has been a significant increase in repo borrowing, indicating a marked increase in long UST securities holdings. Until that point, aggregate hedge fund repo borrowing and lending exposures were generally matched, as one would observe with UST arbitrage strategies such as trading on-the-run/off-the-run spreads or yield spreads (see Figure 2). The divergence between hedge fund repo borrowing and lending is likely driven by a significant increase in recent years in UST cash-futures basis trading (see Figure 3). As with many other spread trades hedge funds engage in, these trades are primarily “short liquidity,” and perform worst in states of the world in which liquidity is scarce. In addition to liquidity risk, such trades also implicitly take on a directional bet on volatility risk and default risk—all three of which spike during periods of market turmoil and economic uncertainty.

Figure 2: Security flows, cash flows, and exposures associated with trading and funding a long-short bond spread trade. Such trading positions can be exposed to liquidity risk, volatility risk, default risk, and repo rollover risk.[i] Source: KMPW.

UST-trading Hedge Funds During March 2020

In March 2020—as investors around the world engaged in a flight to cash and liquidity amid an unprecedented, sudden economic shutdown—there was a sharp divergence in the UST spreads that hedge funds generally bet will converge. We find the average hedge fund with UST holdings in our sample experienced a return for that month of around −7%. We show that by the end of March 2020, the average hedge fund with UST exposures significantly reduced their gross exposures and arbitrage activity in UST markets, decreasing notional exposures on both the long and short sides by around 20%. Surprisingly, despite the fall in UST exposures, borrowing levels and collateral rates on bilateral repurchase agreements—the primary source of financing for hedge fund UST holdings and cash-futures basis trades—remained relatively unchanged in March 2020 for the average hedge fund. Although significant negative returns depleting their equity, hedge funds held leverage ratios largely unchanged, indicating that they scaled back their exposures proportionately to the declines in asset valuations. At the end of March, funds held 20% higher cash holdings and smaller, more liquid portfolios.

In aggregate, we do not find evidence that UST hedge funds provided liquidity during the market dislocation. We drill down further to analyze the effects on hedge fund liquidity provision during this crisis stemming from creditor constraints, redemption risk, and margin pressure.

Dealer Regulatory Constraints and Bilateral Repo Lending

There has been much debate about the impact of post-GFC regulations on UST and other fixed income market liquidity and the impact of dealer constraints on hedge fund arbitrage activity.[ii] Hedge fund arbitrage trading implicitly depends on dealer balance sheets because it requires funding that is typically provided by dealers. Dealer balance sheet and risk management constraints can therefore potentially limit the provision of liquidity by hedge funds, particularly in times of stress.

However, in our granular analysis using hedge fund-dealer level borrowing data, we do not find evidence that the sell-off in UST in March 2020 was driven by a credit supply shock stemming from the regulatory constraints of dealer banks. In fact, we find that G-SIBs—which face enhanced regulations and are often taken as the dealer set more constrained by regulations—provided over 11–13% higher repo funding compared to other dealers during the crisis to hedge funds. Contrary to the regulatory constraints hypothesis, the largest dealers that are subject to enhanced prudential regulations provided disproportionately better access to funding to their hedge fund counterparties during this period of market stress.

There are several possible reasons why broker-dealers affiliated to banks subject to enhanced regulations were able to disproportionately increase repo funding to connected hedge funds in March 2020. These dealers are larger and more diversified, and therefore have a greater risk-bearing capacity. Their regulated status can give them greater access to cheaper funding, which is further augmented during crisis periods via Fed facilities such as the Primary Dealer Credit Facility (PCDF).[iii] The temporary exemption of UST securities from leverage ratio charges is also likely to have boosted G-SIB dealers’ liquidity provision in UST markets around the COVID-19 shock. In addition, during the turmoil, these institutions—subject to enhanced regulations constraining their liquidity and risk-taking, greater disclosures, and periodic stress tests conducted by the Fed post-GFC—were not exposed to significant run risk, unlike during the GFC. This may have mitigated precautionary liquidity hoarding behavior by bank-affiliated dealers.

Redemption Restrictions and Investor Runs

The boost to precautionary liquidity holdings and the step back from UST market activity were less pronounced for funds with lower redemption risk due to longer (stricter) share restrictions including lock-ups, gates, and redemption notice periods, which can dampen the pace and volatility of redemptions in times of stress. We find that hedge funds with higher redemption risk (shorter share restrictions) increased their precautionary liquidity holdings to a greater extent during the March 2020 market stress episode. Such UST trading funds traded out of and closed out more portfolio positions, and cut their UST exposures by more. Funds with less stringent share restrictions likely expected higher contemporaneous and anticipated future outflows and hence, anticipated a greater need for ready liquidity to meet redemptions.

In our sample, the share restrictions of the median hedge fund are such that the fund would have at least 30 days’ notice before the first 1% of investor capital (net asset value) is redeemed. In a short-lived market dislocation like in March 2020, the long share restrictions employed by hedge funds were likely stabilizing, allowing funds to hold onto more of their convergence trades without engaging in fire sales to meet large investor outflows.

Overall, we find that the reduction in hedge funds’ UST exposures is consistent with a flight to cash and precautionary hoarding of liquidity amid increased uncertainty and anticipated future redemptions.

Basis Trading and Margin Pressure

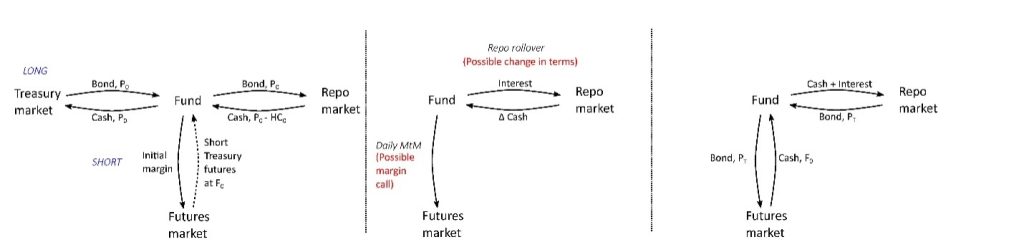

Compared to other UST trading funds during the March 2020 turmoil, the subset of UST hedge funds that predominantly engaged in the cash-futures basis trade faced greater margin pressure stemming from their short futures positions, requiring immediate liquidity infusions or position liquidations. We find that basis trading funds decreased their UST exposures and repo borrowing to a greater extent amid worsening terms, including shorter maturities and higher haircuts compared to other UST hedge funds. Basis traders’ cash positions including posted margin were substantially higher. Also, basis trading funds reduced the number of open positions in their portfolios more than other hedge funds. These findings are consistent with basis traders facing greater immediate liquidity needs and funding pressures.

Figure 3: Security flows, cash flows, and exposures associated with trading and funding the cash-futures basis. Such trading positions can be exposed to liquidity risk, volatility risk, repo rollover risk, and basis risk.[iv] Source: KMPW.

How Did the Funding Structure and Liquidity Management of Hedge Funds Compare to That of Other Asset Managers?

During a systemic stress period, asset managers face a trade-off: selling the more liquid assets first likely has a smaller price impact and mitigates current realized losses. However, such an approach to liquidity management makes the remaining portfolio less liquid, increasing the risk of fire sales should the crisis persist or worsen, with adverse implications for fund performance and financial market functioning. On the other hand, selling illiquid assets earlier, while potentially incurring greater current realized losses, improves the liquidity condition of the fund in the future, when the crisis might deepen. Therefore, the pecking order of liquidity risk management by hedge fund managers has important implications for financial stability.

We find evidence of the latter approach being used by the hedge funds in our sample—funds with UST exposure significantly increased both their cash holdings and the liquidity of their portfolios by reducing the size of their portfolios and disproportionately scaling down relatively illiquid assets. These shifts were likely primarily driven by the consideration of future redemptions. Although the period of extreme market stress lasted less than three weeks before the Fed’s unprecedented intervention—too short a period for hedge fund investors to redeem their shares en masse given the long lockups of the typical fund—we find that it resulted in a precautionary flight to liquidity, likely motivated in part by concerns about future investor redemptions. This precautionary flight to cash was less pronounced for funds with longer (more stringent) share restrictions.

Certain characteristics of hedge funds may increase their financial fragility. For instance, compared to other asset managers such as mutual funds or money market funds, which are subject to regulatory constraints regarding portfolio liquidity and leverage, hedge funds tend to hold more illiquid portfolios, use greater leverage, and have a more concentrated investor base. Hedge funds can attempt to manage these structural risks by imposing stricter share restrictions, holding greater precautionary cash, or increasing the maturity of their financing. We show that hedge funds are quick to significantly increase their unencumbered cash holdings and portfolio liquidity when faced with severe market stress. Longer share restrictions were particularly useful for UST trading hedge funds during the sell-off in March 2020, allowing them to avoid fire sales and hold onto more of their convergence trades, thereby bolstering both fund and market stability. As we discuss further in the paper, our findings illustrate a crisis episode during which the liquidity management and funding structure of hedge funds likely were more stabilizing than that of mutual funds (which do not have share restrictions and were subject to significant investor outflows) and money market funds (which were subject to potentially destabilizing contingent liquidity restrictions).

Following the March 2020 Turmoil

We find that hedge fund UST trading exposures did not revert to their previous levels after the market turmoil subsided, even as the average UST-trading hedge fund saw returns jump back in April and remain positive over the subsequent months. Notably, in the post-shock period, UST funds faced greater investor outflows, but met those redemptions in a market stabilized via Federal Reserve interventions. Our findings indicate that the quick intervention of the Federal Reserve to stabilize Treasury markets likely prevented a deleveraging spiral in which hedge funds would have further sold off positions in a declining market, likely realizing greater losses and further depleting their equity.

[i] A common case study on the risks inherent in arbitrage trading is Long-Term Capital Management (LTCM), which engaged in such bond spread trading until a systematic shock caused massive losses that threatened systemic stability and led to a Fed-arranged broker takeover of the fund’s positions (Edward (1999); Jorion (2000); Lowenstein (2000); Duarte, Longstaff, and Yu (2007)). Industry insiders and observers drew parallels between the 1998 LTCM episode and the impact of the March 2020 shock on fixed income hedge funds. There are indeed some parallels, but, as we point out in the paper, also important distinctions between the two episodes.

[ii] See, for example, Duffie (2020); He, Nagel and Song (2020); Schrimpf, Shin, and Sushko (2020).

[iii] The set of primary dealers’ parent companies overlaps significantly with the set of G-SIB institutions (see Table B.1 in KMPW).

[iv] In this trading strategy, a hedge fund goes long the (cheapest-to-deliver) Treasury security and goes short the corresponding Treasury futures contract. The futures leg does not require reverse repo, so the divergence between hedge fund repo borrowing and lending is consistent with reports of a significant increase in recent years in UST cash-futures basis trading. Typically, this is a low volatility, low yield convergence strategy that is operationally intensive and requires leverage to be worthwhile. The trade is profitable as long as the actual cost of carrying the cash position (the “repo rate” or the cost of repo borrowing for the hedge fund) is below the implied cost of carry on the futures (the “implied repo rate”).

Mathias S. Kruttli is at the Board of Governors of the Federal Reserve System

Phillip J. Monin is at the Board of Governors of the Federal Reserve System.

Lubomir Petrasek is at the Board of Governors of the Federal Reserve System.

Sumudu W. Watugala is at Cornell University, SC Johnson College of Business.

This post is adapted from their working paper, “Hedge Fund Treasury Trading and Funding Fragility: Evidence from the Covid-19 Crisis,” available on SSRN. The views stated herein are those of the authors and are not necessarily the views of the Federal Reserve Board or the Federal Reserve System