For an industry built around “diversification,” we still have plenty of work to do to apply the concept to our investment teams. We know that if you restrict a portfolio, you can’t always maximize performance, so isn’t it reasonable to consider that the same might hold for talent diversity and team performance?

The composition of investment management teams is suboptimal in terms of diversity – particularly gender diversity – the focus of this study. In my study, women make up only 1 in 7 investment professionals, while other studies report the proportion drops to 1 in 10 for portfolio managers. In my recent paper, I find that diversifying teams by gender improves subsequent fund performance for actively-managed US equity funds.

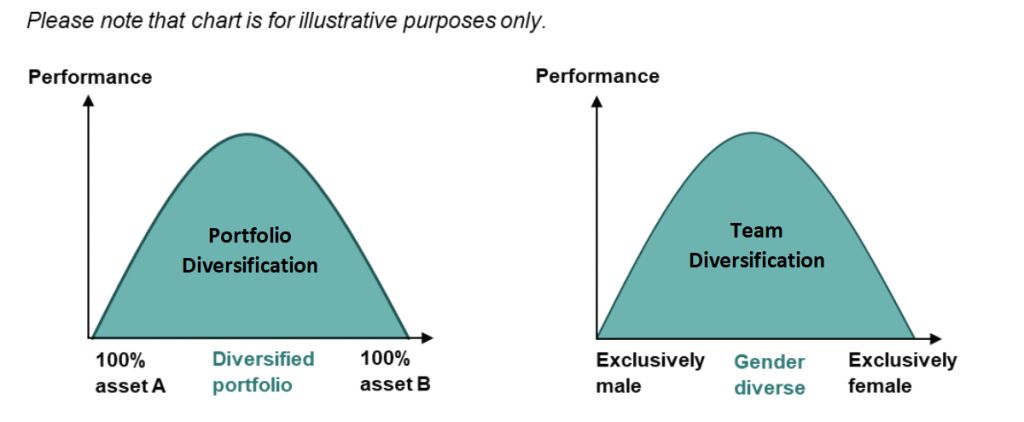

Figure 1 visualizes my research findings in reference to standard portfolio diversification theory.

Figure 1: Fund performance – from portfolio diversification to team performance

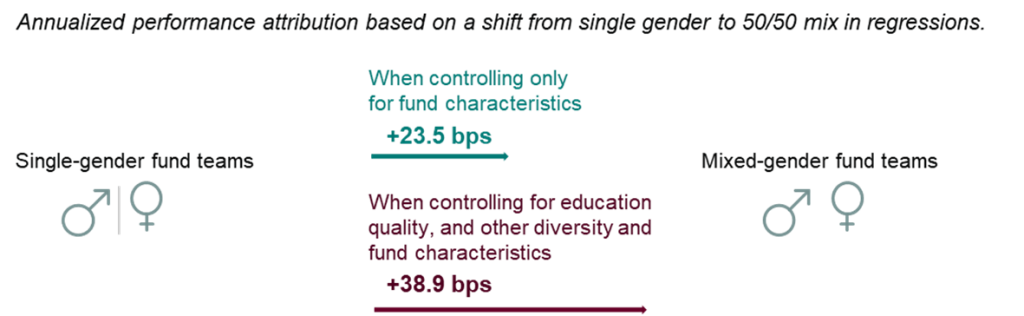

Empirically, my research shows that gender diverse investment teams outperform single gender teams by as much as 38.9 basis points annually when also considering education quality and other forms of diversity, such as diversity of thought that might arise from studying different subjects at different universities in different countries. Gender diversity plays an incrementally important role when building high performing fund management teams that cannot be explained by education, professional designations or other characteristics of the investment professional, the team or the fund.

The value of diversity in teams has been demonstrated repeatedly, starting with experiments in the 1960s that showed teams of diverse individuals outperform more homogenous teams on a wide range of tasks. If you want to improve performance, the research suggests building a team of individuals who have different backgrounds, education, and professional training. Yet, we frequently bias towards sameness, overlooking opportunities for diverse interactions and the associated performance improvements.

A Novel Approach to Measuring Team Diversity

To explore how investment teams benefit from gender diversity, I had to overcome two challenges: First, the ambiguity in how teams are defined. Second, a lack of completeness in diversity information.

Expanding the definition of “teams”

Most studies of mutual fund performance focus on the “named professionals” – the senior portfolio managers whose names are explicitly included in regulatory filings and fund prospectuses. However, many portfolio management teams rely on a variety of other key players – analysts, traders, and business executives associated with the fund, to name a few.

To the extent that additional professionals play a direct role in the formulation of investment strategy, their attributes – including quality (such as their education, qualifications, and experience) and diversity – should reasonably play an important role in performance.

My research goal was to understand to what degree gender diversity among investment management teams can impact fund performance. To accomplish that, I leveraged detailed data of 2,669 U.S. activity equity funds from eVestment, a global database of investment managers and fund offerings. The data includes details about other investment professionals on the team, making it possible to see whether gender diversity beyond named Portfolio Managers bore any relationship to fund performance. In doing so, I found that a balanced team of equal gender representation has the potential to improve fund performance by as much as 38.9 basis points per year, even after controlling for other dimensions of diversity, such as international experience, the diversity of thought represented through different degree programs and colleges, and professional qualifications – information readily available in biographies.

Using natural language processing to overcome bias when identifying gender

A big concern when working with data on team composition is completeness. If information is incomplete, the analysis can suffer from data gaps and systemic biases. In the case of eVestment, investment firms are encouraged to voluntarily submit information on diversity, but a significant fraction of managers choose not to submit these statistics, often citing privacy concerns. Using this information to make inferences about team diversity is less than ideal, so instead we leveraged the supplied biographies of team members. Over 90% of investment professionals associated with actively managed investment funds include a personal biography. These biographies provide detailed information about the employment history of the employee, their education (including degrees attained and the granting institution), and gender as indicated by their preferred pronouns. By using preferred pronouns instead, I explicitly avoid the implicit bias of similar academic studies where gender is inferred from the first name and its implied gender.

Natural Language Processing (NLP), the use of computer algorithms specifically trained to parse plain text into machine consumable insights, can transform biographies into specific data points. Well documented programming packages and techniques can be used to quickly transform sentences into their component parts of speech (such as pronouns), named entities (such as academic institution) and relations (such as identifying which university granted which degree). For the purposes of this research, those data points focused on the education and gender of each investment professional.

Figure 2: Example of entity resolution and pronoun identification in biographies

Relating Performance to Gender Diversity

The core of the study looks at the 1-year performance (in excess of the fund’s benchmark) for actively-managed US equity mutual funds over each month of the period 2008 to 2021 and seeks to relate it to characteristics of the fund and the composition of the team.

The simplest way to accomplish this is to separate funds by the gender composition of the team and note any systematic difference in performance across these groups. I find that all-male teams underperform the average by 12 basis points and all-female teams underperform by 6 basis points. Meanwhile mixed gender teams show outperformance of 10 basis points.

A more rigorous way of exploring this relationship is to use regressions to control for other characteristics of the fund, such as fund size and turnover, and the team, including team size, educational diversity, and professional qualifications. I perform a series of regressions that test whether gender diversity still explains the subsequent shift in performance after adding these controls. While there may be other dimensions of diversity that are important, we are leveraging the information we have at our disposal in the biographies and controlling for as many other factors as possible.

When we look solely at gender diversity, controlling for general fund characteristics, a shift from single-gender teams to gender-balanced teams results in a 23.9 basis point performance improvement.

Controlling for the educational quality of the team further enhances this relationship. We proxy for quality with Ivy League education as an unambiguous representation that has an enduring tie to rigorous degree programs and selective student acceptance. When we control for education quality and all other fund and team characteristics, gender-balanced teams outperform single-gender funds by 38.9 basis points.

Figure 3: Performance change attributable to gender diversity

Source: Vanguard, “Diversity Matters: The Role of Gender Diversity on US Active Equity Fund Performance,” Data from eVestment, LLC.

Implications for the Investment Management Industry

Investors looking to maximize their returns might consider funds run by teams with well qualified, diverse investment professionals. Our results suggest that the fund industry should look to improve investment performance by improving gender diversity as an added attribute of well-qualified, well-trained, diversely experienced investment teams.

With women comprising only about 1 in 7 U.S. active equity investment professionals, the fund management industry may have an unrealized opportunity to increase performance.

To aid in increasing gender diversity in such roles, the investment industry may benefit from additional research on the dynamics underlying current findings. The approach used in my paper could be extended to help us understand the importance other key dimensions of diversity. For example, questions remain about how different genders approach risk taking; the interaction of diversity, seniority, and performance; and the impact of equity and inclusion in helping to retain talent and reduce employee turnover.

This research challenges anyone involved in investment management to approach team diversity with the same rigor we do portfolio diversification, recognizing the meaningful impact both have on fund performance.

Stephen Lawrence is a Senior Investment Strategist for The Vanguard Group.

This post is adapted from the paper, “Diversity Matters: The Role of Gender Diversity on US Active Equity Fund Performance,” available on SSRN.

The views expressed in this post are those of the author and do not represent the views of the Global Financial Markets Center or Duke Law.